Insurance industry trade groups lauded the U.S. House of Representatives’ vote on Nov.

14, reauthorizing the National Flood Insurance Program (NFIP). The 21st Century Flood Reform Act (H.R. 2874) would reauthorize the program for five years and enact operational changes.

Advocates from RIMS, the risk management society, the Property Casualty Insurers Association of America, and SmarterSafer.org also asked that the Senate waste no time in passing its version of the measure before its expiration on Dec. 8.

On Sept. 8, President Trump signed legislation passed by both houses to extend NFIP authorization until Dec. 8, which previously had been set to expire Sept. 30.

Dow Jones reports that the act’s reforms include:

- Authorizing $1 billion to elevate, buy out or mitigate high-risk properties

- Capping flood insurance premiums at $10,000 per year for homeowners

- Removing hurdles to the private flood insurance market, which often offers better coverage at lower cost than the NFIP

- Providing for community flood maps and a homeowner’s ability to appeal their flood designation

- Better aligning NFIP rates to match a property’s true risk, particularly for in-land and lower-value properties

- Improving the claims process for flood victims

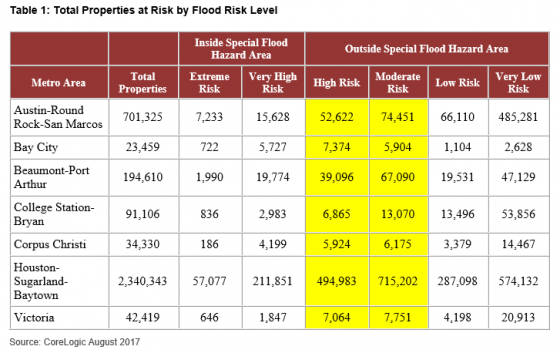

- Addressing repeatedly flooded properties, which account for 2% of NFIP policies but 25% of claim payments

While it applauded the U.S. House of Representatives for deciding to reauthorize the NFIP, RIMS, the risk management society, also urged the Senate to quickly follow-up before the program’s Dec. 8 expiration. Allowing the NFIP to expire would have “significant repercussions, impacting both corporate and residential property owners,” said RIMS Vice President Robert Cartwright Jr.

“Nearly five million American consumers rely on the NFIP to protect their homes, properties, and businesses,” said Nat Wienecke, senior vice president of federal government relations at the Property Casualty Insurers Association of America (PCI). “A long-term reauthorization is needed to provide consumers and markets with reliability and stability when it comes to flood insurance coverage.

”

SmarterSafer.org, a coalition of taxpayer advocates, environmental groups, insurance interests, housing organizations and mitigation advocates, said in a statement that this year’s “historic hurricane season has pushed the nation’s debt-ridden flood insurance program past the point of bankruptcy once again, so we applaud the House for passing a legislative package that reforms the NFIP to ensure the program is financially sustainable for the future.” The organization also lauded the House for investing in recommended measures including “mapping and mitigation, addressing affordability and providing consumer choice in the flood insurance marketplace.”

The NFIP was created more than 50 years ago to provide affordable flood insurance as private insurers pulled out of the market. The program’s large debt led Congress to cancel $16 billion of its debt last month. NFIP now has about $6 billion to pay claims and $10 billion left that it can borrow from the Treasury Department, according to the Federal Emergency Management Agency, which manages the program.

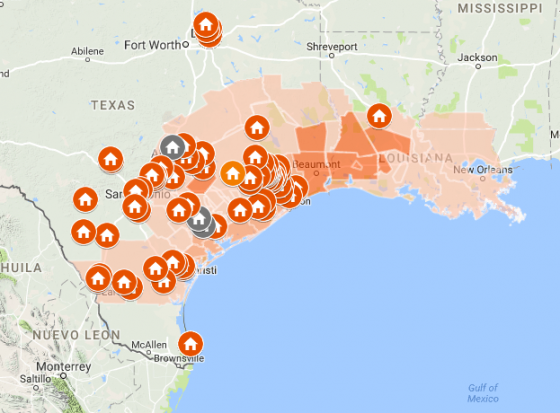

Hurricane Harvey, which made landfall in Texas on Friday night as a Category 4 hurricane, has so far caused at least five deaths and more than a dozen injuries. Now a tropical storm, Harvey has dumped more than 30 inches of rain on the Houston area, with another 15 to 20 inches anticipated by Friday.

Hurricane Harvey, which made landfall in Texas on Friday night as a Category 4 hurricane, has so far caused at least five deaths and more than a dozen injuries. Now a tropical storm, Harvey has dumped more than 30 inches of rain on the Houston area, with another 15 to 20 inches anticipated by Friday.

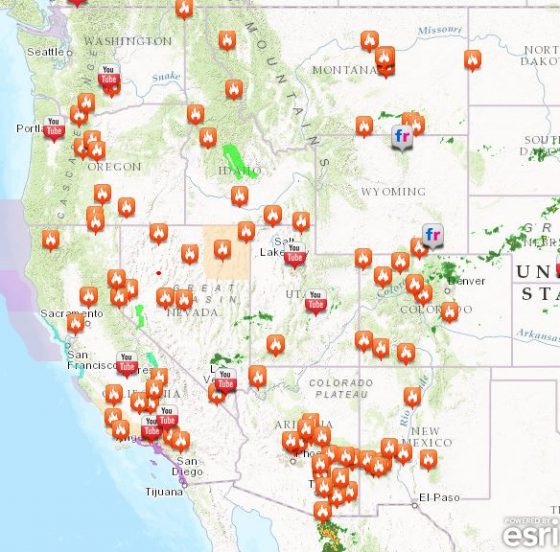

Western Canada is also seeing its share of wildfires. Evacuations are in effect for up to 10,000 residents in British Columbia, as 17 fires burn.

Western Canada is also seeing its share of wildfires. Evacuations are in effect for up to 10,000 residents in British Columbia, as 17 fires burn. Residents of Fort McMurray, Canada, who saw

Residents of Fort McMurray, Canada, who saw