Examining a matrix of variables affecting a state’s insurance regulations, the R Street Institute determined that Vermont has the best regulatory system for insurance and that  North Carolina has the worst, according to the Insurance Regulation Report Card.

North Carolina has the worst, according to the Insurance Regulation Report Card.

The annual report grades each state across seven dimensions. The three fundamental questions the report seeks to answer are:

1. How free are consumers to choose the insurance products they want?

2. How free are insurers to provide the insurance products consumers want?

3. How effectively are states discharging their duties to monitor insurer solvency and foster competitive, private insurance markets?

“We believe states should regulate only those market activities where government is best-positioned to act; that they should do so competently and with measurable results; and that their activities should lay the minimum possible financial burden on policyholders, companies and, ultimately, taxpayers,” Senior Fellow R.J. Lehmann said in a statement.

According to the report:

The insurance market is both the largest and most significant portion of the financial services industry to be regulated almost entirely at the state level. While state banking and securities regulators largely have been preempted by federal law in recent decades, Congress reserved to the states the duty of overseeing the “business of insurance” as part of 1945’s McCarran-Ferguson Act. On balance, we believe states have done an effective job of encouraging competition and, at least since the broad adoption of risk-based capital requirements, of ensuring solvency. As a whole and in most individual states, U.S. personal lines markets are not overly concentrated. Insolvencies are relatively rare and, through the runoff process and guaranty fund protections enacted in nearly every state, generally quite manageable. However, there are certainly ways in which the thicket of state-by-state regulations leads to inefficiencies, as well as particular state policies that have the effect of discouraging capital formation, stifling competition and concentrating risk. Central among these are rate controls.

For the third straight year, the report found that Vermont had the best insurance regulatory environment in the United States, receiving the only A+ score. Other states receiving either an A or A- were Arizona, Idaho, Illinois, Kentucky, Maine, New Hampshire, Utah and Wisconsin.

Meanwhile, North Carolina had the worst score, receiving a failing grade for the third year in a row. States ranking a D include Alaska, Massachusetts, California, Hawaii, Louisiana, Mississippi, Delaware, Montana, North Dakota and New York.

R Street found the most significant shift to be the continued expansion of North Carolina’s two property insurance residual market entities, even as Florida’s Citizens Property Insurance Corp.—previously the nation’s largest residual market entity—has continued to shrink.

“Not coincidentally, when R Street issued its first regulation report card in 2012, Florida ranked dead last and North Carolina was somewhere in the middle. This year, North Carolina is dead last and Florida is somewhere in the middle,” Lehmann wrote.

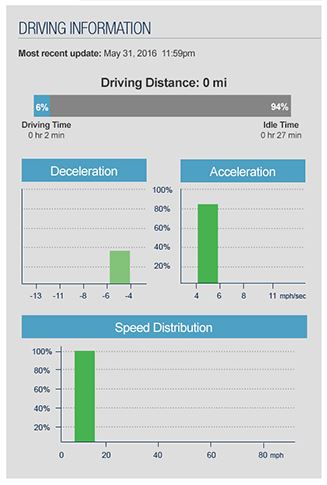

about driving behavior—insights that can shed light on a driver’s risk category. In a further innovation, 2016 brought the establishment of a telematics data exchange, enabling risk managers to make use of this data with the consent of drivers.

about driving behavior—insights that can shed light on a driver’s risk category. In a further innovation, 2016 brought the establishment of a telematics data exchange, enabling risk managers to make use of this data with the consent of drivers.

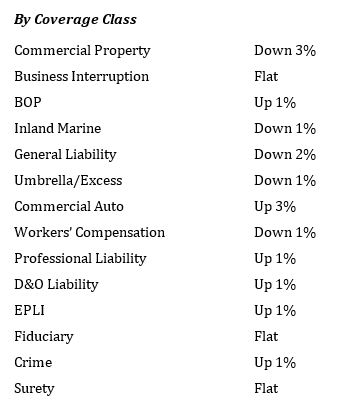

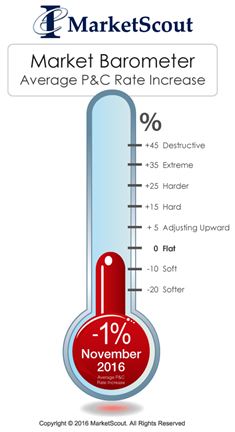

according to MarketScout.

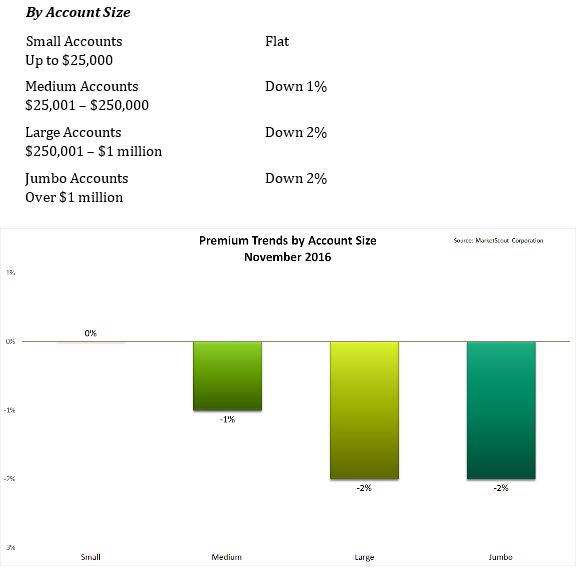

according to MarketScout.