CALGARY, ALBERTA, CANADA—Suppose your company experiences a major hurricane, tornado or fire: Property is destroyed and your business is stalled, meaning customers are left waiting.

But there are buildings to be rebuilt and equipment to be replaced, and the claims process hasn’t even started. This is when the risk manager’s skills at placing the company’s insurance coverage and negotiating for the best payout can not only demonstrate their true value, but can put the company back on course, according to experts here at RIMS Canada’s annual conference.

“When there’s a serious property loss, this is the time for the risk manager to shine, because up until then it’s about premium, premium, premium,” Tom Parsons, manager of risk management at Fairmont Raffles Hotels International in Toronto said during a RIMS Canada Conference session. “Up until a serious loss occurs, I don’t think you feel the impact that you can give back to the company. Because what we do is buy insurance, so it has to work.

It is what you helped craft and build into your policy through the years. You have created a policy that is robust, and that is going to cover everything—you hope.”

Among the examples cited was a soft drink bottling plant flooded with eight feet of water following a hurricane. While the company’s high-speed bottling equipment was damaged and would need to be replaced, explained Jeffrey Phillips, managing director in PwC’s U.S. forensic advisory practice, the issue was that floodwaters were highly contaminated due to a number of chicken and hog farms in the area. As a result, the company determined that the building could not be used for any type of food processing and would need to be demolished. The insurer, however, argued that the walls could be sealed, containing any contaminants. The company had found a competitor to do some of the bottling, but it wasn’t enough to fill their orders, Phillips said.

Because delivery of the new bottling equipment was slated to take months, there was also a large business interruption period being covered, he said. This is when innovation came into play. The bottling company was able to show the insurer that buying another plant rather than rebuilding would put them back in business sooner, cutting back on their losses. The insurer agreed and sent them a check. As a result, the company purchased a larger facility in a better location.

“They were up and running in six months—the business interruption had stopped,” he said. The better location also meant reduced shipping costs and the company gained market share. Because the company was able to make the case to its insurer, both came out ahead in the long run.

Phillips recommended that companies negotiating after a crisis “communicate, communicate, communicate” with their insurers.

They should also get their insurers to sign off on major contracts such as scope of work, rates and overhead and discuss changes to operations or facilities with the adjustment team and agree on scope of property damage repair or replacement whenever possible.

Insurers will typically push to return the facility to pre-loss condition, “unless you can prove the changes will save them money,” he added. “Insurers will not be creative for you, they don’t know your business or your goals.”

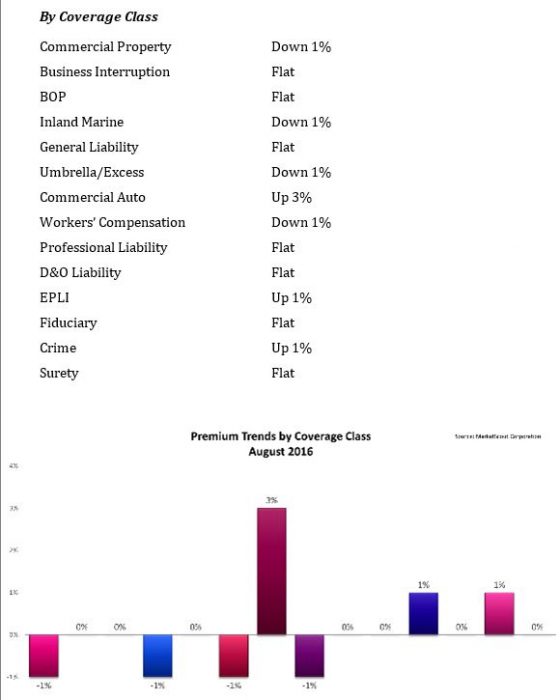

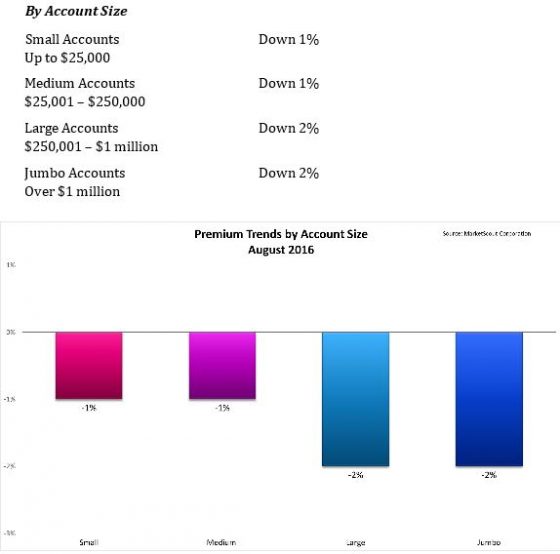

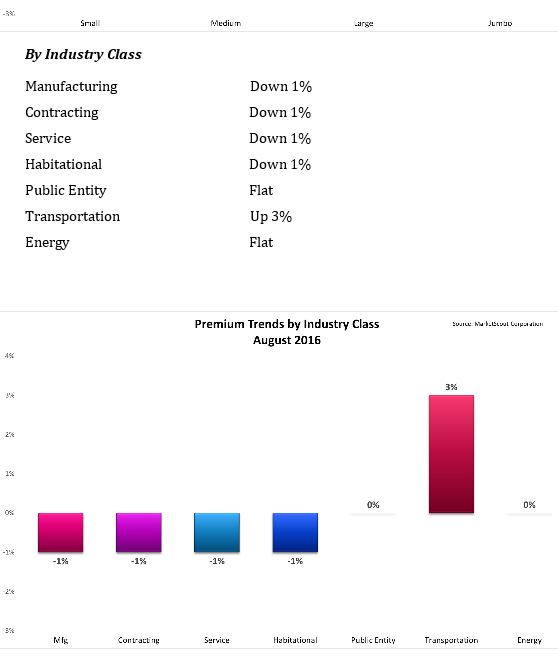

industry classifications remained unchanged.

industry classifications remained unchanged.